While one can argue that India might resort to further easing of rates, the following points are noteworthy:

- Market yields mostly run ahead of actual rate cuts, tuning in to market cues and inflation expectations.

- The RBI has paused rate cuts and seems to prefer using more innovative tools such as the Operation Twist and long-term repo operations instead, to manage borrowing costs and liquidity

This essentially means that whether you lock into deposits or lock into quality bonds today, your return prospects will suffer from low interest income or low capital gains or both. If you decide to search for higher interest rates, you may have learnt by now from DHFL and Yes Bank that they do not come without risks at this juncture. This is true of high yielding mutual funds too. This does not mean you should stay away from debt entirely. Please read our recommendation part to know when and how to use debt.

Time for equity

When it comes to asset allocation, adding when everyone’s fearful is the best maxim to follow. Equity certainly makes the cut today as there’s plenty of pessimism in the markets, with people taking a negative view of every event.

Here’s why we think this is good time to start raising your equity allocations and start deploying surplus cash if any.

- India is one of the few countries to actually gain, over the medium term, from the oil price wars that have sent crude oil to sub$40 levels. According to reports a $5 per barrel change in crude oil per year can bump up India’s GDP by 25 basis points, arising from lower current account deficit. The relief arising from lower crude prices can be quite significant for the economy and for companies using petro-linked inputs too. Industries spanning transportation, logistics, auto, cement, airlines, FMCG and paints will benefit from lower input prices with margin improvements from favourable crude prices.

- The coronavirus assault has ended the uncertainty about whether global central banks will launch another round of rate cuts and stimulus. The US Fed by cutting rates by 50 basis points has already set this motion. If the present global mood of easing rates to rescue economies from coronavirus continues, that’s a boost for global liquidity which will find its way into India through the FPI route. As things stand, India is better placed than many emerging nations, in terms of impact from the virus outbreak.

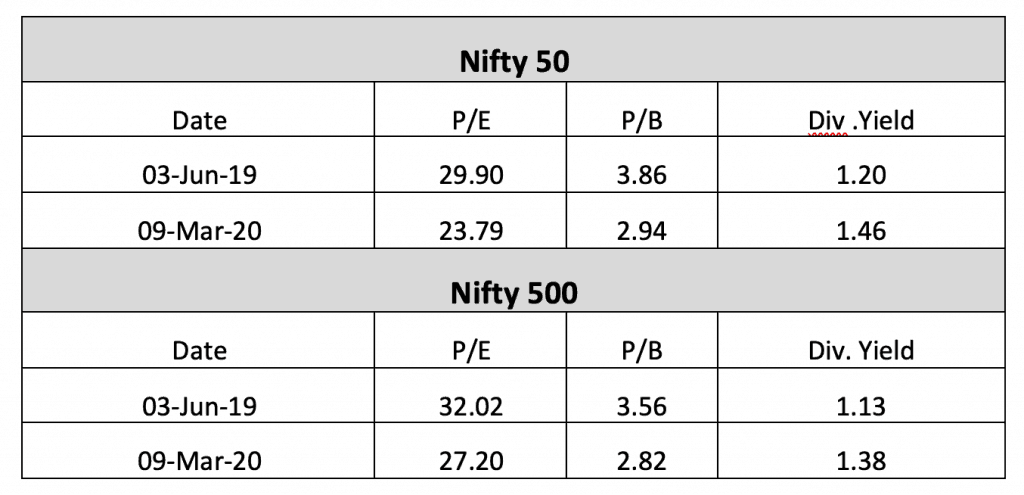

- India’s market valuations, seen from a price-book perspective are not as expensive as they were in previous market tops. While price to earnings went far lower during the 2008 correction, the price to book ratio remained elevated. From a peak of 6.5 in January 2008, it still remained an average 4.2 times for whole of that year (it hit a low of 2.1 in October 2008 before recovering). To this extent, the Nifty’s price to book value of 2.9 times and the Nifty 500’s 2.82 times today, offer some comfort that markets are not abnormally expensive. Do also note that while certain segments of the market have participated in this bull market and are expensive still, others have mainly sat on the sidelines and are already at attractive valuations. Not all sectors or stocks in the market bottom out at the same time.

Phased allocations

But if the time for allocating more to equity is here, should you deploy your entire cash or jump in with lumpsums right now? Our answer is to go in for phased deployment owing to the following:

Contained but not insulated: As things stand today, the coronavirus spread in India appears contained. But then the global impact has become too serious for India to say it is cocooned from the impact. When SARS broke out in 2003, China accounted from 4.2% of world economy. It now makes up 16.3%. Next, with Europe and US reporting serious virus breakout numbers, the impact in India cannot be isolated, global monetary easing notwithstanding. The volatility and downside from this will persist for some weeks or months and India will not remain unaffected.

Not a massive correction: The correction of 15% for the Nifty 50 and the Nifty 500 from the past peak of January 17, 2020 are hardly a blip from a historical perspective. In 2008, for instance, the Nifty 50 was trading at 23 times just a month after the correction began and went as low as 10.7 times in October 2008. Currently, after the correction, the Nifty valuation is at 23.79 times. This must also be seen in conjunction with the present earnings situation. The turnaround in earnings in September and December 2019 has largely been driven by banks. The Yes Bank issue could place a speed-breaker to the sector’s earnings recovery, as contagion effects play out and depositors and fund providers for banks go through risk aversion mode.