Equity index funds are meant to track markets passively and not built to necessarily beat active funds. But if you had an Indian index that is able to beat comparable active funds with consistency, generates strong return, adds diversification to your portfolio and even substitute some categories of active funds, would you not consider it?

It is the Nifty Next 50 index. This index is made up of the 50 biggest stocks beyond the Nifty 50. In effect, it is the Nifty 100 stocks less the Nifty 50. The Nifty Next 50 is a great addition to long-term portfolios for these reasons:

- One, it beats the Nifty 100 and the Sensex Next 50 across timeframes. It even often manages to deliver returns better than mid-cap indices such as the Nifty Midcap 100 in longer timeframes.

- Two, its sector allocation is more diverse than the Nifty 50 and is less heavily weighted towards a few key sectors such as financials.

- Three, most active large-cap funds have struggled to deliver better than the Nifty Next 50 in longer-term periods. Several multi-cap funds, too, in recent years, do not fare well when compared with the index.

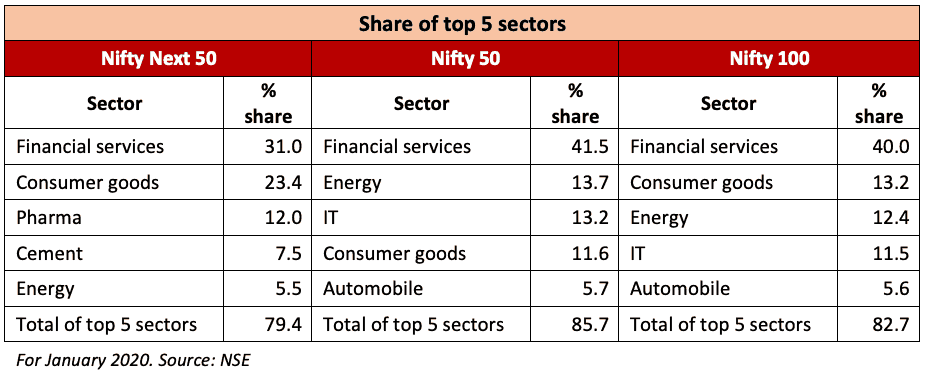

Diffused sector presence

The Nifty Next 50 (Next 50) has wider stock and sector coverage than the Nifty 50 and is more evenly distributed (see table) compared with the Nifty 100 as well.

While the Next 50 is also dominated by financials, the index has a significant contribution from other sectors such as consumption and pharma. Its consumption exposure has, for example, helped its strong performance in the past years while the relatively lower cyclical sector share helped contain losses. On the financials side, it’s not just banks – the index constituents include insurance and other finance companies.

Capturing the growth

The Next 50 has the unique ability to capture a stock’s growth as it gets larger and larger to eventually make it into the Nifty 50. This is partly why the Next 50 is able to deliver extremely well during market upswings. The Nifty 100, while also housing these stocks, is far more diffused with lower individual stock weights, while the Next 50’s small set provides focus.

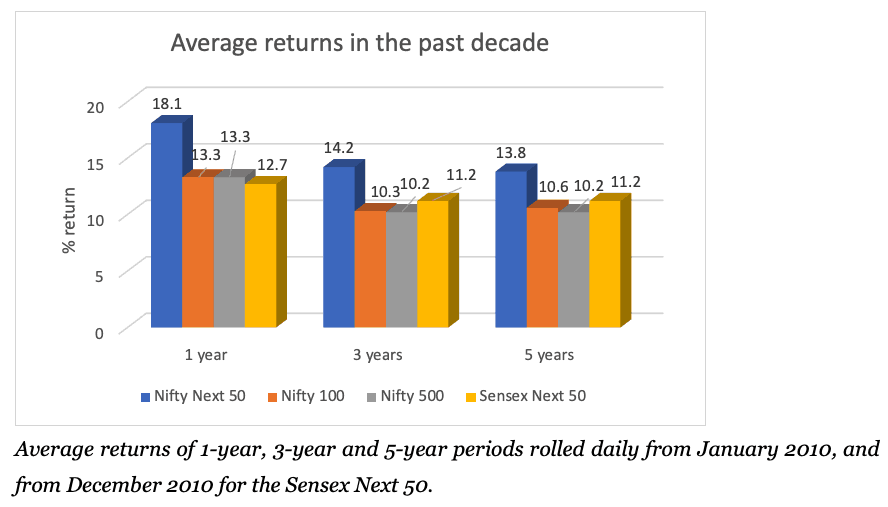

Average returns of 1-year, 3-year and 5-year periods rolled daily from January 2010, and from December 2010 for the Sensex Next 50.

Rolling the 3-year returns for the past decade, the Next 50 beats the Nifty 100 over 70% of the time. Stretching the period to 5 years, the Next 50 beats the Nifty 100 over 90% of the time. That’s a high degree of consistency in delivering better returns. The closest comparable, the Sensex Next 50, pales in performance.

The Next 50, despite being made up of large-caps alone, additionally beats the broad-market Nifty 500 all the time on a rolling 5-year basis, and close to 90% of the time on a rolling 3-year basis since 2010. In fact, the Next 50 sports a far better upside capture ratio.

Beating active equity funds

Recent underperformance of large cap funds aside, on a rolling 5-year returns in the past decade, the Next 50 still beats these funds over 70% of the time.

And it is not just large-caps that struggle. One in two multi-cap funds, too, tend to trail the Next 50 more often than they are able to beat it in the 3-year and 5-year periods.

Suitability

The index’s return drivers during market rallies also contribute to its underperformance in phases, such as the present one.

The poor 1-year performance compared with the Nify 100, for example, is a factor of the index’s lower weight to banking, which has been a star sector in the recent market rally. Two, because it has a relatively higher individual stock concentration compared to the Nifty 100, underperforming stocks such as Indiabulls Housing, Hindustan Zinc, and Aurobindo Pharma serve as a bigger drag.

The Next 50, therefore, is a much more volatile and therefore higher-risk index. In market corrections, the Next 50 fares poorly. For example, the worst 1-year loss for the Next 50 was 67%, against the 57% of the Nifty 100. In fact, the downside capture for the index is similar to that of pure mid-cap indices.

The Next 50, therefore, is meant only for long-term horizons of at least 5 years to allow volatility to play out. The index can be used in any of the following ways:

- One, as a substitute for a large-cap fund, or part of multi-cap exposure only by high-risk investors.

- Two, by moderate risk or conservative investors who want a substitute for aggressive midcaps.

- Three, by investors who want diversification in their long-term portfolios.

- Four, mix with value-based strategies as the index is a “growth” style index.

Funds and ETFs to invest in

The index is well-represented in the mutual fund and ETF space. Here are our picks:

- ICICI Prudential Nifty Next 50: This is the index fund we prefer. We chose this over the other Next 50 funds as it has a history enough to check tracking error, an important metric in index investing. We are also closely watching the UTI Nifty Next 50 which is performing well on all fronts but has a limited track record.

- Nippon India ETF Junior Bees: If you have a demat account, you can invest in this ETF. This ETF has among the most consistent and high trading volumes and value among those that track the Next 50. While ICICI Pru’s ETF comes close to Nippon, its trading volumes are far more erratic. Nippon Junior Bees also has a large asset size.

33 thoughts on “Prime Recommendation: An equity index that challenges active funds across categories”

Hello, I just joined as paid member. I was looking at other qualitative parameters in your portfolios especially standard deviation and some sort of measure of risk when compared to the market and govt bonds at the overall portfolio level. Can you please detail some more on them in order to assess and compare with what I already have.

I am invested in the following currently: Nifty: 20%, Nifty Next 50: 30%, Reliance Pharma fund: 4% and Reliance small cap 6% for equities and ICICI short term debt – 40%. Separately, I have a put aside money needed for 5 years of expense and once in every 5 years I will redeem funds to furnish my next 5 years of expenses.

How do my investment portfolio compare with your active portfolios on return and risk parameters. I am 50 years of age and would want my investment portfolio to outlive me, hoping that I will not have to withdraw no more than 4% in any given year. I already have 5 year buffer to take care of market volatility.

Hello sir,

Can you please write to us separately here: https://staging.primeinvestor.in/contact-us/. For specific querires such as this, we prefer this route.

Thanks,

Bhavana

Hi Bhavana,

Good one. The Prime rating was given as 2.0 for ICICI Pru Nifty Next 50 Index Fund. But for NIFTY index funds given 4+ rating.

Prime rating is different from recommended picks in this article. Can help elaborate why difference is ?

Hello,

The rating in the case of index funds is tricky and very different from the other fund categories. We measure performance metrics of each index fund against the underlying index – so tracking error, for example, is taken for each fund against its own index. At the time of scoring for the rating itself, we put index funds together. This does not mean that we’re comparing the returns of different indices. Index funds are different in that we aren’t trying to measure how much it can deliver, we are measuring how efficient that index fund is. So Ipru Next 50 scores low because other nifty index funds, for example, have lower tracking error or lower expense ratio.

As we’ve mentioned in the article, we are watching the other Next 50 index funds for tracking since they are new but come with lower expense ratio. Up until a 1-1/2 years ago I Pru Next 50 was the only viable option for the Next 50 index. There was IDBI Next 50, but has a very low AUM and very high tracking error.

Thanks,

Bhavana

Hi Bhavana,

Is mixing Nifty next 50 fund with Nifty 50 index good idea? E.g. large cap exposure with 70% Nifty next 50 fund and 30% Nifty 50 fund?

Hello,

Yes, you can mix Nifty 50 and Next 50. There are other indices that you can use too…we have a passive portfolio here: https://staging.primeinvestor.in/prime-portfolio-details/?id=10. You can take cues from this portfolio too.

Thanks,

Bhavana

Madam please write about STRUCTURED PRODUCTS and their purpose

Hi Bhavana,

Value Research rates the ICICI Pru Nifty Next 50 as 3 Star ( 2 Star for Direct Plan) with the Trailing returns given below:

Trailing Returns (%)

YTD 1-Day 1-W 1-M 3-M 6-M 1-Y 3-Y 5-Y 7-Y 10-Y

Fund -0.52 -1.12 -2.63 -2.97 -0.16 8.28 10.39 5.41 7.78 13.24 —

S&P BSE 100 TRI -0.75 -0.62 -0.28 -2.50 1.43 9.21 12.86 11.39 7.81 12.33 —

The Fund seems to have underperformed the S&P BSE 100 TRI for 1 Year, 3 Year and 5 Year trailing periods. Does not seem to be in sync with the chart you have published. Where have I gone wrong?

Hi Sridhar,

The chart shows average return across timeframes, i.e., it is average of all 1-year, 3-year, and 5-year return periods from Jan 2010 to Feb 2020. (mentioned in the note below the chart). The returns you see in Value Research is the point-to-point returns of one single period, such as Feb 2019-Feb 2020 (1-year return), Feb 2017-Feb 2020 (3-year return) and so on.

In the past year, the Nifty Next 50 has been underperforming the Nifty 100 because of some stocks sliding (please see para under Suitability section) and these stocks relatively having higher weights than in the Nifty 100.

Hope this answers your doubts.

Regards,

Bhavana

Yes it does. Thanks Bhavana

Hi Bhavna,

One question I had with respect to Index funds versus ETF. In my current portfolio, I have a mix of both and I was wondering whether you have a recommendation between the two. What are they uniquely suited for and in the current juncture what is your recommendation; choose index, ETF or a combination?

Would appreciate your guidance.

Hi Rahul,

The choice is not only index or only ETF. It depends 🙂 there are good ETFs with no index fund alternatives, so you will have to necessarily go with the ETF – and vice versa. Two, in some cases, while there could be an ETF, it may not have enough volumes. For example, there could be a mid-cap ETF that has poor volumes and therefore, index fund would be the better option.

Three, it also depends on what you’re comfortable with, where you have good ETFs and index funds. If you don’t mind managing your portfolio when it includes both ETF and mutual funds (for example, sometimes, you may hold MF in one platform and ETF in another, so it may get cumbersome), then it is fine to go with a combination.

Thanks,

Bhavana

Thanks, Bhavana. Appreciate your response. Got it.

On volumes, is there a site where we can review the volumes for a period. Or ss the fund size a good proxy for the volumes. Thanks!

Hi Rahul,

You can find volumes on NSE’s site. Put in the ETF name in the input field to get the ETF page, and you will have historical data including volumes there. Larger fund sizes are always preferable to smaller ones.

Thanks,

Bhavana

Thanks, Bhavana

Dear Bhavana

Great article! John Bogle would be proud how Indexing is catching on in India.

One question: I am investing in ABSL MidCap fund (Direct plan). Can I consider ICICI Pru Nifty Next 50 as a proxy to that MidCap fund and invest in it? It comes with lower expense and with all benefits of indexing. Your position seems to favour this (replacing a midcap with NN50). Any guidance would be helpful.

Best regards

Naren

Hi Bhavana, there is a lag in comments posted on the website due to intermediate moderation. Hence, I did not see your earlier recommendation on combining NN50 with a Value fund.

As suggested by you, I have been combining ICICI Pru Nifty Next 50 with ABSL Pure Value fund. Hope this is a good strategy.

Naren

Hi Naren,

Yes, we do sometimes take time to approve a comment, as we’d rather reply to it while approving. We don’t want to accidentally miss answering questions! Anyway, yes, combining Next 50 and a value fund will be a good strategy. But in your case, note that ABSL Pure Value has a high share of mid-caps and small-caps – it will be more volatile than other value funds. It’s one of the reasons that fund fell very sharply in the 2018-2019 correction.

Thanks,

Bhavana

Hi Naren,

There are instances where the Next 50 beats the mid-cap index…but good mid-cap funds beat the mid-cap index. So if your risk appetite is high enough to allow a pure mid-cap fund, you should ideally combine a mid-cap and the Next 50. Using the Next 50 will work if you are conservative but still want upside capture.

Thanks,

Bhavana

Hi,

Is Holding both NN50 Index fund and a aggressive midcap fund like Kotak Emerging Equity in the portfolio right approach, if risk is acceptable ?

Hello,

Yes, you can hold both funds in the same portfolio if your horizon is 5+ years at the minimum. If you can, do combine the Next 50 with a value-based fund.

Thanks,

Bhavana

My observations so far :

The last 10-15 stocks of NN50 is midcap stocks, may be this is the reason the performance is better than Large cap funds.

Why no fund manager is using NN50 as benchmark to select the stocks to build their funds(Multicap).

Is it kind of Midcap or multicap fund ?

Hello,

Nifty Next 50 is a large-cap index. It is a subset of the Nifty 100 index. The reason you’re seeing mid-cap stocks there is because some stocks have fallen very sharply and this has eroded their current market cap. The cut-offs for market cap definitions are based on averages over a period and not as on a particular date. These stocks that are just below the large-cap cut-offs cannot be constituted as a true mid-cap in terms of behaviour or risk. That kind of mid-cap exposure is much further down the market-cap curve, even in midcap funds. The Next 50 does not benefit from mid-cap exposure. For funds, the Nifty 100 is often the benchmark since it is a broader and closer representation of the universe large-cap funds invest in. Multi-cap funds tend to have indices such as the Nifty 500 as they invest across market caps.

Thanks,

Bhavana

Hi Bhavana,

Two questions:

a) UTI Nifty Next 50 has an expense ratio of 0.27% and ICICI Pru Nifty Next 50 has an expense ratio of 0.39%. What’s your rationale for recommending a more expensive fund?

Also, I was a bit surprised that you did not mention expense ratios in your analysis.

b) These funds invest 68% in giant and 23% in large cap funds. So, over 91% in giant and large cap funds. However, the performance seems to be still better than the Nifty 100 by quite a bit. Of course, the delta has to come from portfolio mix being different. Can you please help to explain this delta a bit more?

Thanks!

Hello,

a) As we’ve explained in the post, we are watching UTI Next 50 – because it has a limited history, we can’t check for tracking error very well, which we can do with ICICI Pru Next 50. We’d prefer not to go by expense ratios alone, as it can change. While expense ratios are factored into our analysis, our argument in this recommendation was more focused on the potential of the index rather than the fund or ETF.

b) The performance difference comes from the gains the index clocks in market upswings – in these markets, stocks rally significantly and rallies tend to be higher outside the main Nifty 50/Sensex. The Next 50 catches these “newer” stocks, and manages to capture the bulk of their rallies.

Thanks,

Bhavana

Comments are closed.