Prime Funds is our recommended list of funds across equity, hybrid, and debt categories. We draw up this list with Prime Ratings as a base, adding more quantitative and qualitative factors on top of it. We review this list on a quarterly basis to ensure that recommendations remain only in quality funds.

In this article, we’re giving the list of changes and the reasoning behind these. You can view the full updated list here.

In this quarter’s review, we have added and removed funds in some categories as explained below. Please note the following:

- Where we have removed funds, we have explained what you should be doing with your investments. So if you hold a fund we have removed from the list, ensure that you read our explanations.

- Funds we’ve removed are not outright poor performers. The reason for removing them may be several and includes: slippage in performance, change in its risk levels, change in a fund’s strategy that may negate the reason why we picked it, change in our outlook about the market and whether such a fund would fit it, or simply if there is an upcoming better performing fund.

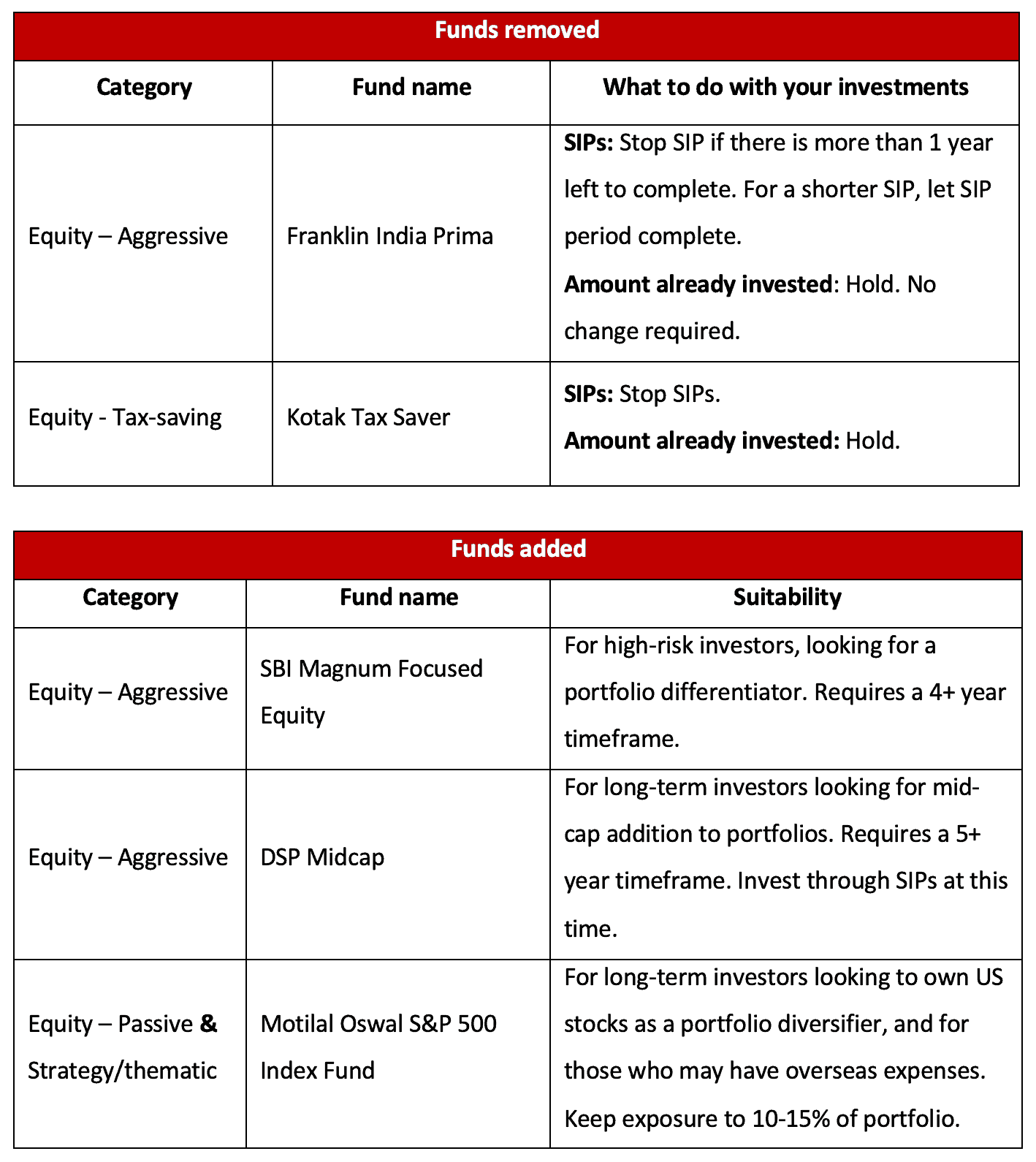

Equity funds

Following is the list of changes. We have explained these changes in detail after the table

Check out the full list of our best mutual funds!

This article talks only about the changes to our Prime Funds list. Don't forget to check out the full list of 48 funds!

Rationale for changes: Equity – aggressive

We removed Franklin India Prima here, owing to it falling behind other mid-cap funds. This fund is, overall, among the less aggressive mid-cap funds as it sticks to the higher end of the mid-cap range. However, its long-term value-based buy-and-hold strategy has not worked well of late. Other funds have also been improving their own performance and moving ahead of Franklin Prima.

The economic impact of the lockdown and pandemic is uncertain at this time. While opportunities remain in mid-caps and small-caps, we’d prefer to stick to quality portfolios available at a reasonable price simply because the pay-off may be faster. Fresh investments in this scenario, therefore, are avoidable. We will be watching this fund’s portfolio and performance to check on potential improvement in prospects. For those who need to stop SIPs (please see table), the SIP can instead be started in other mid-cap funds in Prime Funds – Kotak Emerging Equity or DSP Midcap.

In the mid-cap space, we added DSP Midcap as it has been steadily improving over the past two years. It has a structured growth-at-reasonable-price approach to picking stocks, looking at earnings growth and classifying stocks based on fundamentals and valuations to arrive at clear buys. Its portfolio spans a wide variety of sectors which can help keep up returns given the lack of clarity on where opportunities will now emerge. The fund is slightly less aggressive than our other mid-cap recommendation, and tends to hold fewer small-cap stocks than its peers. The fund is suitable for long-term investors who wish to include mid-caps in their portfolios.

Focused funds are a good diversifier to a portfolio as these funds take concentrated bets and follow a bottom-up strategy, unlike other multi-cap funds. This was among the reasons to add SBI Focused Equity. A good fund in this space, its portfolio is almost evenly split between mid-caps and large-caps. This gives it access to opportunities across the market, unlike most other focused funds that tend to have a higher large-cap share. SBI Focused Equity often picks offbeat stocks across a range of sectors; it is also adept at exiting stocks indicating that it has the ability to realise gains made. The fund has been steadily improving performance, and sports lower volatility and better risk-adjusted return than peers. However, the fund suits only high-risk long-term investors given the nature of strategy and mid-cap orientation of portfolio.

While this is not a change, a word on HDFC Small Cap’s performance. This fund has also seen performance pale in comparison to category toppers. However, this partly stems from its portfolio’s higher allocations to cyclical sectors and other sectors such as hotels that have been hurt in this correction. The fund’s portfolio, however, still looks reasonably diversified. It also remains among the few steadier options in the small-cap space. We are watching the fund’s performance and portfolio changes.

Rationale for changes: Equity – tax saving

We removed Kotak Tax Saver as it has seen performance start to dip over the past few months; the margin by which it was earlier able to beat the category average and the Nifty 500 TRI has been shrinking. Its consistency has also seen a dip. Further, funds in this category – apart from the top few – are also showing increasing inconsistency. That is, few funds are able to steadily remain above-average and few funds have a consistent market-cap allocation.

Given this, we’ve decided to keep the recommended list short and go only for stable and top funds. The purpose of this category is extremely specific – tax saving. To this extent, our view is that it is sufficient to have a few quality, steady funds. A wide variety of strategies and high returning funds is not really needed here.

If you have SIPs in Kotak Tax Saver, you can opt for either of the Prime Tax-saving funds.

Rationale for changes: Equity – passive & Strategic/thematic

We added Motilal Oswal S&P 500 Index, a brand-new index fund (it’s still in its NFO period). This inclusion comes from the S&P 500’s strength in providing diversification to any long-term portfolio and its access to global businesses. Compared to the Nifty 50 and the Nifty 500, which are key Indian indices, the S&P 500 is far more diversified. The index has beaten the Nifty 500 TRI over 3 and 5 year periods; the rupee depreciation against the dollar can also add to return. US and Indian stock markets also have low correlation, and this proves a good hedge.

The S&P 500 index fund is suitable for long-term investors (5+ years) looking to diversify into overseas markets, or those who may have expenses such as a child’s education expenses abroad. We have also included this fund in the strategic/thematic section to ensure that those who are not interested in passive funds do not miss this opportunity. Please note that fund details for this fund will be available after the NFO period.

More aggressive investors or those who want to own US stocks for their strength in information technology can go for the Motilal Oswal Nasdaq 100 FOF. We have, in this review, included this fund in the passive fund category. This fund continues to be part of our strategic/thematic section in Prime Funds.

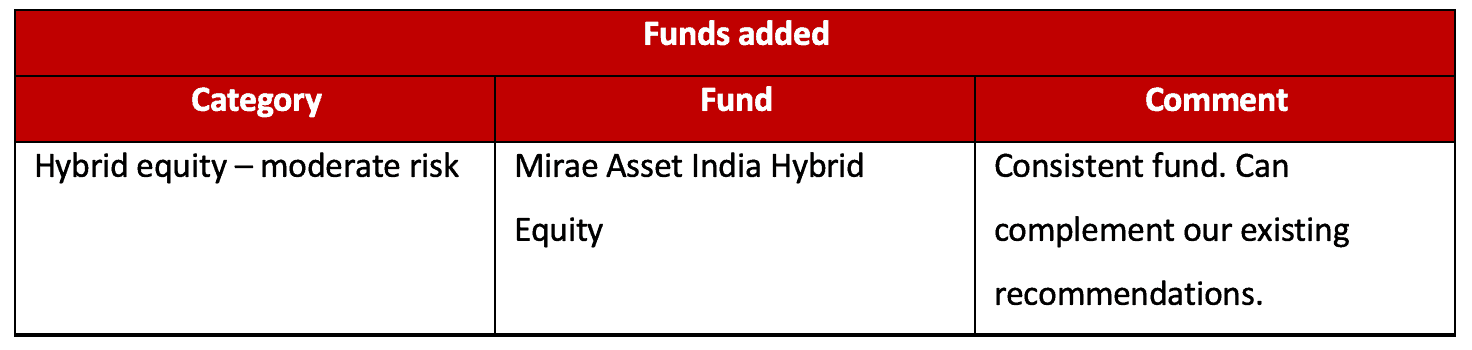

Hybrid funds

Following is the change made to this category:

Rationale for changes: Hybrid Equity – Moderate Risk

We added Mirae Asset Hybrid Equity to provide some balance to the value-tilt in some of the other funds in our list. The fund has been a consistent performer, beating peers 80% of the times when 3-year returns were rolled daily over a 6-year period. While its top stocks mirror Mirae Asset Largecap, some differences in individual stock and sector allocations sets it apart. The fund has a clear large-cap and growth tilt. It appears to have a sedate medium-term debt portfolio with 17% in gilt and remaining in quality bonds. The fund can be held as a large-cap asset allocated substitute for an equity-heavy portfolio.

While there are no other changes in this category, we would like to take note of marginal slippage in the performance of both HDFC Hybrid Equity and ICICI Pru Equity & Debt. This we attribute to the partial value tilt in both these portfolios and value as a strategy not particularly doing a great job of containing downside at this point. Investments and SIPs in the funds can continue as the portfolios do not point to any undue concerns.

Hybrid equity – Low Risk

There are no changes in this category. We would like to take note of the fact that ICICI Pru Balanced Advantage has not done its best in terms of containing downsides in recent times. This was due to higher net equity position it held compared with peers such as DSP Dynamic Asset Allocation.

We are not averse to the ICICI fund’s strategy of higher equity position if the downsides are better contained than regular equity funds. The fund’s fall is still far lower than that of the aggressive hybrid category. We are also watching DSP Dynamic Asset Allocation closely as it has moved up in our ratings. However, over a rolling 1-year period, the ICICI fund continues to outpace the DSP fund.

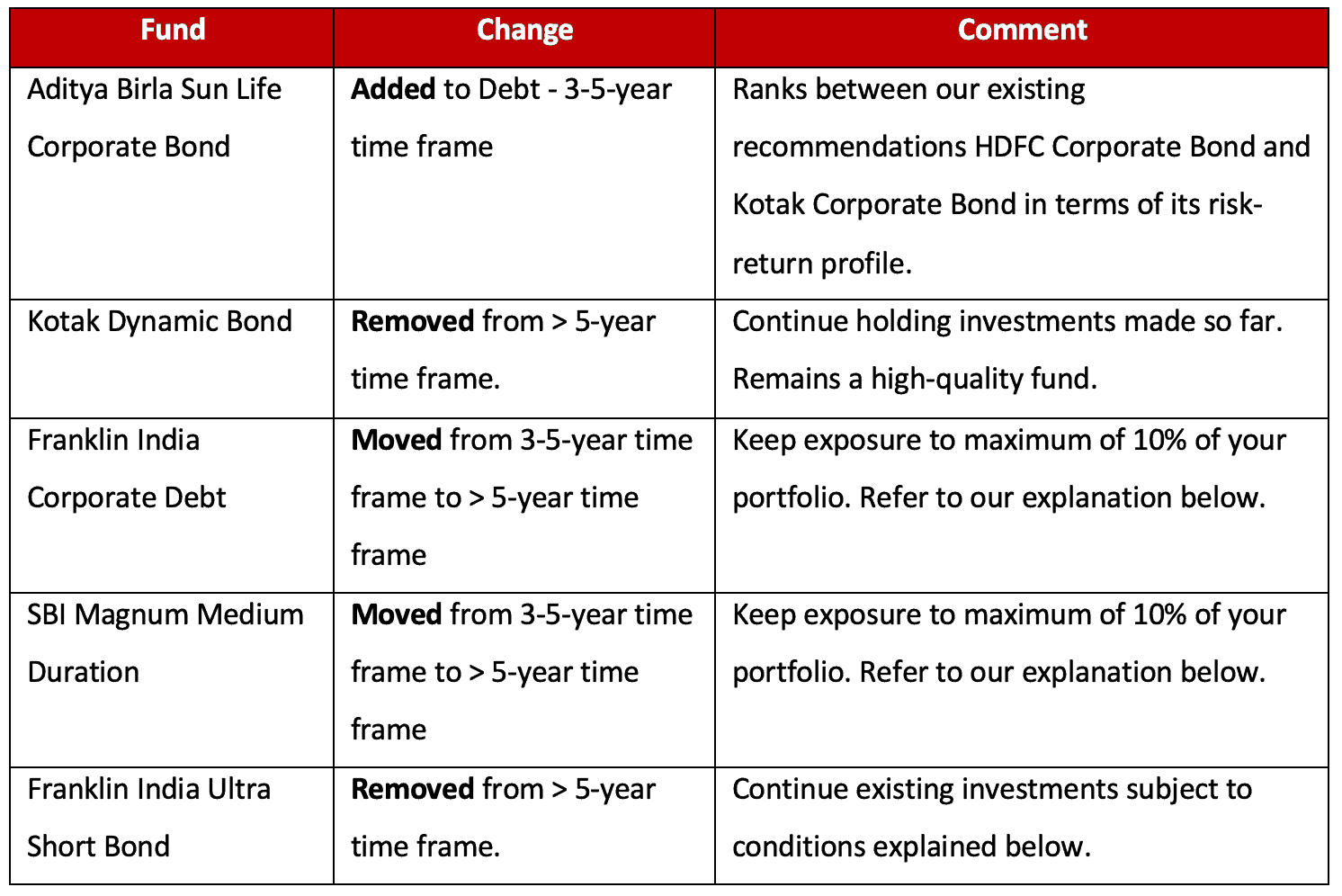

Debt funds

We are treating debt with caution (both on the credit and duration front) at this juncture. We recently gave a call of 3 funds for a low interest scenario.

Every time we give such recommendations, we have queries from you on whether you should change the funds we already have in our portfolios to the ones we recommend. This is not needed. We will sound you off when we make changes to our portfolios. Also, whenever we give such calls, you need to make sure they align with your time frame. It cannot be simply about ‘best funds to invest in’.

With that, following are the changes made to debt funds:

Rationale for Changes: Medium term – 3 to 5 years

This is the bucket that most investors seem to prefer for debt. At this juncture, when there is heightened risk of credit deterioration, we decided to keep very high-quality funds in this bucket and therefore added Aditya Birla Sun life Corporate Bond fund. This fund had a history of being a short-term fund pre-2018 but post moving to this category has maintained a 2-3-year maturity. With almost nil exposure to papers less than AA+ credit rating, the fund has beaten peers 84% of the times when 1-returns were rolled daily.

Rationale for Changes: Long term – Above 5 years

We removed Kotak Dynamic Bond from our over 5-year time bucket as we do not want to take the dynamic bond strategy at this stage of uncertainty. We will retain SBI Magnum Constant Maturity which has a far clearer long-only gilt strategy and zero credit risk.

Please note that Kotak Dynamic Bond continues to score well on all metrics. Our call now is simply to stick to funds where we know what to expect in terms of duration than go for a dynamic strategy. We may re-introduce the fund at a later juncture. Much of Kotak’s non-gilt exposure will be available in our corporate bond recommendations. You can continue to hold the fund.

We moved both Franklin India Corporate Debt and SBI Medium Term Duration to the greater than 5 years space for 2 reasons: one, with an average 14% and 37% exposure respectively to instruments below AA+ rating, both these funds had a higher risk profile than peers.

Two, while we have clearly stated that these have a higher element of risk in our ‘why this fund’ explanation, we want to make sure that only very long-term investors pick these funds to handle the risks. Franklin India Corporate Debt has high exposure to single corporate group, although with high credit rating. Such concentration, in our research methodology, ups the risk profile. In the case of SBI Medium Duration, while overall risk profile is higher, it is mitigated by diversification across a large number of instruments.

Investors in these funds need to note 2 things:

- You need to have at least a 5-year time frame so that the fund can recover from any hits if it transpires.

- If you are already invested for a 3-5 year timeframe, make sure these funds do not individually account for over 10% of your portfolio.

If either of the above is not true, please use our Prime Funds to move into debt funds that suit your time frame or where exposure is very high, reduce exposure to the above and diversify.

We are removing Franklin India Ultra Short Bond from our above 5 years bucket and shifting it to a ‘hold’ recommendation with some conditions. Even while asking investors to pare exposure to Franklin India Ultra Short Bond as early as November 2019, and again in January 2020 we had retained Franklin India Ultra Short Bond in our over 5 years’ time frame. We did this because the fund has over the past 5 years shown ability to recover from any hits in a year or two. This comes only because of the high yield and mispriced opportunities that this fund relentlessly pursues as a strategy.

However, we understand from many of your queries that you either have an exceedingly high allocation to this fund or have a lower time frame for this fund, not sufficiently aware of its risks. The search for high returns without understanding risks is a perilous path. We would rather not take the chance at this juncture of heightened credit risk by trying to explain the risks. We would rather remove the fund altogether.

Avoid further exposure to the fund. If you hold the fund, you can continue to hold it as its risk-return profile over the long-term remains favorable. However, it is subject to the following:

- The fund should not account for over 10% of your portfolio.

- If you are running SIPs, you may do so as long as its exposure is within this limit in your overall portfolio.

If either of the above is not true, please use our Prime Funds to move into debt funds that suit your time frame.

For funds that we have removed from Prime Funds but feature in Prime Portfolios, we’ll be reviewing and updating the portfolios next week.

You can view the full updated Prime Funds list here.