Most of you are now comfortable with the fact that gilt funds can deliver negative returns in the short to medium term when rates move up. We have also written about it here. But the negative return prevalent in the past month or so, across most categories in debt funds has troubled many of you.

In our last debt fund call, we discussed the volatility in debt returns and what should be your course of action. But many of you are concerned about the fall in short and medium duration fund categories – especially in our recommendations across floater, short duration and corporate bond funds. This article will explain why this is happening, whether it is normal and what you should do.

Before we go to reasons, you need to remember the fundamental characteristic of your debt fund’s return. As yields move up the prices of bonds fall. This is sharper in longer duration bonds and gentler in lower duration bonds. But the price fall is inevitable when yields move up – until funds adjust to the new yields by acquiring bonds with higher coupon.

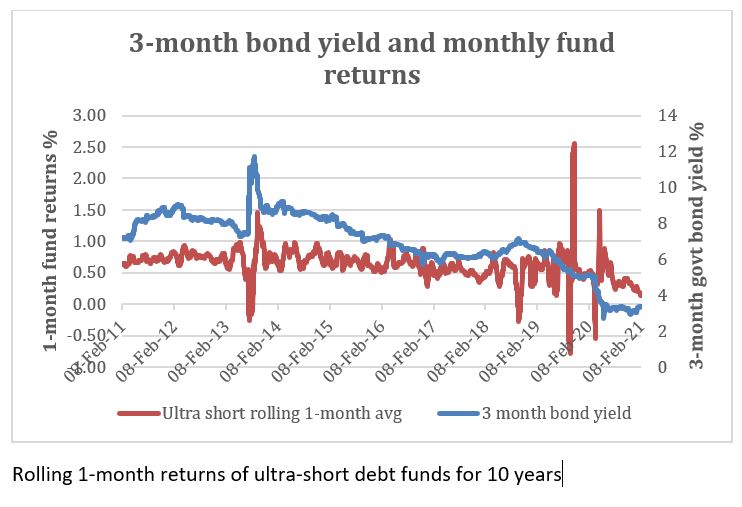

The graph above will tell you that after the unusual, very short-period, rise in yields in March 2020, bond yields fell steadily, stabilised but started climbing up from end November 2020. Some ultra-short and low duration (which are the comparable funds for the above bond tenure) funds did make marginal negative 1-month returns but have now bounced back (due to RBI OMO activity).

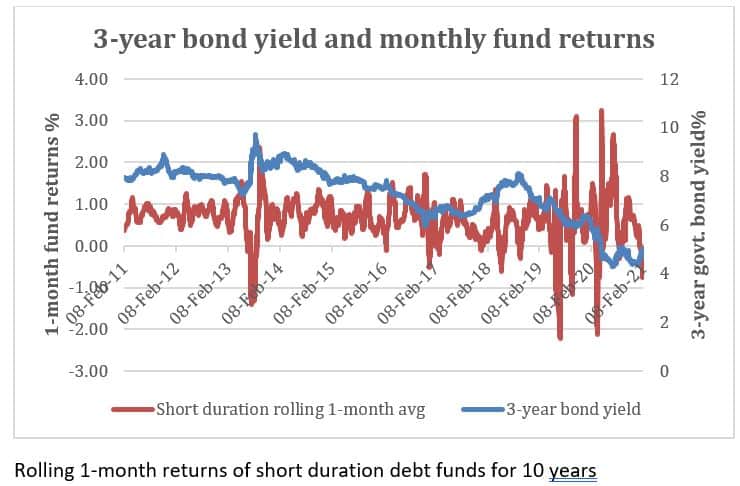

In medium and long-duration bonds, you will see that the move was different. The 3-year yield fell sharply and since January 2021 rose sharply – causing 1-month losses in your short duration, floater, banking & PSU and importantly corporate bond funds.

Takeaway: Your debt fund returns will rise when yields fall. When yield moves up, there can be losses. When the yield up move is gentle, you feel less pain. When it is sharp, it is a lot more painful. A very sharp up move for just a couple of days of March 2020 is case in point.

Gear up for more volatility

If we agree that rate up moves should cause a fall in your debt fund returns, then the next question should be, how bad can the fall be? We can refer to previous cycles here.

When yields bottomed out in December 2016 and started climbing up – short duration funds fell -1.2% for that month. This was for a 40 basis-point up move in 1-year govt. bond yield. In the past month now, a 20-basis point rise in bond yield caused a -.0.7% fall in short duration funds.

But then there’s evidence that debt fund returns are getting more volatile. Instead of absolute numbers, let’s look at the standard deviation of 1-month returns of some of the fund categories that have been around for a while now.

The data above will tell you that the volatility has gone up. It is significant in lower duration categories than in the already liquid and volatile gilt space. (We have not taken the newer categories of corporate bonds and banking & PSU and they did not exist as a category until 2018).

Beyond duration and credit, there have been other macro changes in the debt market that have caused your debt NAVs to swing more. We list them below:

#1 Regulatory changes

From late 2017, SEBI has been steadily rehauling debt-fund related guidelines. As a result, what was earlier loosely defined in terms of investment universe and valuation has become watertight.

Category changes

SEBI brought in new categories that became effective over early to mid 2018. One of the key elements of the changes was defining the duration of many debt fund categories. Low duration funds for e.g.: needed to have a Macaulay duration (MD) of 6-12 months while the limit for ultra short was 3-6 months. Earlier, such a distinction did not exist and these categories of funds roughly had similar tenures. Similarly, short duration had a MD of 1-3 years.

As a result, the average maturity of some of the fund categories increased to comply with newer norms, making their volatility profile higher than before.

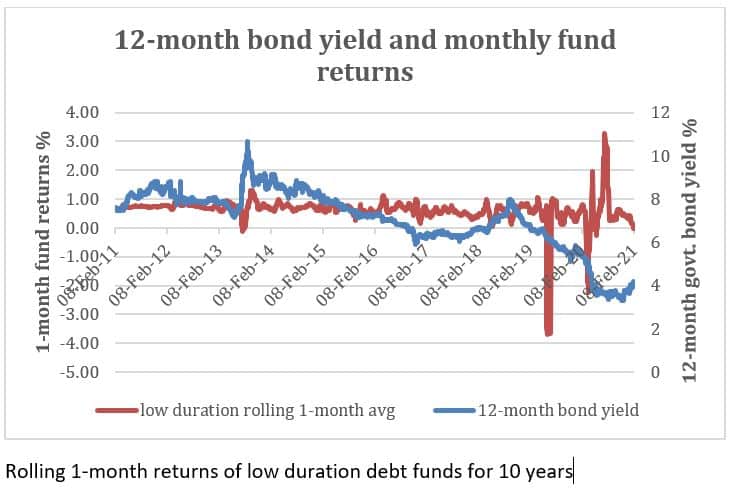

The 3 graphs below will show you the increased volatility in different categories recent years – even as the rate spikes are not sharp (barring the one-off event in 2013).

Bottomline: Funds have less leeway to change duration now and therefore need to take more volatility.

Investment & valuation norms

SEBI also brought in a series of changes in valuation and investment norms for debt funds in 2019. Among those, 2 important changes are: the valuation of debt instruments of over 30 days was made mark-to-market (as opposed to the earlier amortisation method) . Effective April 2020, all instruments were to follow mark to market subject to the guidelines given by SEBI. Second, debt funds could not invest over 10% of their assets in unlisted instruments.

The first-mentioned measure made NAVs more volatile as they were closer to market reality than they were before. The second removed discretion in valuations and ensured better price discovery.

Bottomline: Prices of underlying instruments of debt funds are now linked more closely to market moves and hence show more swings.

#2 FPI activity

Just as in stocks, higher foreign flows in Indian bonds has contributed to the volatility too. The government has been proactive in terms of increasing the allowable limits for FPIs in corporate bonds – raising it to 15% (of outstanding amount) in 2020 from 9% earlier. The table below will show you how the limit has been upped. While the limit hasn’t been fully utilised, the higher FPI participation has given space for a more active bond market and heightened volatility (read quicker price discovery too). Rupee strength and falling rates usually heighten FPI flows (see the limit utilised in 2019).

For you as an investor, the impact of this could be felt across banking & PSU debt, short duration and corporate bond funds as the instruments in these fund categories are typically the ones preferred by FPIs; other than gilt.

Bottomline: Like the equity markets, the debt markets too may gradually see more foreign money driven moves.

#3 RBI’s active intervention policy

From a time when RBI was using the monetary policy to control rates we now have the Central bank actively intervening in markets to provide liquidity and manage government borrowing costs . Apart from ‘open market operations’, RBI used ‘operation twist’ pre Covid to flatten the yield curve.

Post March 2020, it made massive purchases through open market operations and opened special liquidity windows for distressed sectors. This kept rates stable and eased yields after the sharp up move in March 2020. Recently however RBI has provided signals that it would like to gradually normalise it’s exceptional liquidity support to markets, as the economy consolidates post Covid. Sans RBI intervention market yields may move up in response to higher government borrowings and elevated deficits.

Bottomline: As liquidity tightens, the climb in short term yields can trigger volatility.

What this means for you

Very simple. The above triggers are here to stay. Greater room to market forces and more participants mean more volatility. Remember gold? It has become a more volatile asset in the past decade, thanks to significantly increased participation by ETF investors globally.

But this also means your funds are more reflective of reality and do not artificially keep your NAV loaded! So here are the takeaways.

- If yields move up, your funds will react negatively. Such response may be higher than what it was in the past.

- Mark-to-market will mean your NAVs will reflect market realities more than before.

- In a rising rate scenario, short and medium duration funds will re-adjust to newer rates and generate higher coupon (interest) once they have more recent securities added.

- If rates remain rangebound or low, you may still face volatility from FPI moves or from a post OMO – withdrawal syndrome.

As an investor, you need to live with this volatility across categories barring overnight and liquid funds and to some extent ultra-short funds. Simply stick to your original duration in line with your goal instead of trying to see if you should change your maturity to suit rate moves. There is bound to be volatility – long or short. Longer duration is more sensitive than shorter duration. But there is no escaping volatility. Get ready for a new normal. If that sounds too adventurous for you, the government schemes do offer a ready alternative.

Update: You can find rolling returns of many debt funds here in our rolling returns tool.

48 thoughts on “Why your debt funds have negative returns and what to do”

Should one necessarily invest in debt funds as part of Asset allocation?

Can we consider Dynamic Asset allocation Funds (or Balanced Advantage Funds) with a 5 year+ horizon as suitable substitutes for Debt funds in the portfolio, with adequate mitigation of equity risk? Also, please let me know of any other suitable alternatives.

Appreciate a detailed reply.

Regards,

Venkatesh

They are not substitutes and this will answer why: https://staging.primeinvestor.in/should-you-invest-in-balanced-advantage-funds-now/ thanks, Vidya

Informative article. Thanks.

Please recommend conservative hybrid fund, as i could not find it in your fund recommendations.

We find funds in this category highly inconsistent and hence avoid it in my list. You can check in our MF review tool though for the better ones, if you are particular. Vidya

One more addition to above query vidya, does the decline in debt portfolio gives an opportunity for additional allocation and if yes in which schemes considering tenor needs to be more or less permanent or at least 3-7 years. My current portfolio is corporate bonds, credit risk funds, banking and psu debt funds. Thanks…

Debt funds offer less averaging opportunities than equity. But if you wish to – If you will take the risk – decline will work in gilt better than others. But that means investing more and seeing more fall. If you can’t take that corporate bonds. thanks, Vidya

Hi Vidya , Thanks for articulating the complex debt market (new norm) in a simple lay man language. Just 1 query , Considering the volatility is here to stay should an investor continue with Corporate bonds, Credit Risk funds, Banking and PSU, Debt portfolio if intention is to hold for anywhere between 3-7 years or even longer or change the mix with intent to earn higher than FD returns. Appreciate your views…

Thanks! Yes, you can – we are not comfortable with credit risk funds though. Vidya

Maam, a major takeaway – live with volatility in debt funds. Could you advise me regarding type of debt funds to choose. I have invested in two debt funds for long term investment (a corporate bond & a gilt) & two short term debt funds for a period of one year plus. Disregarding the volatility in the short term funds, should I persist with my long term (at least 5 years) choices in the debt funds ?

Yes, of course you can..just take the volatility. That’s all. regards, Vidya

What will a good approach for someone transferring some funds from FDs to debt funds with a long term (5-7 years) horizon with primary objectives being tax efficiency and slightly better returns?

Just invest across ultra short, short and medium duration prime funds. This will ensure duration volatility is reduced. thanks, Vidya

Hi : very nice article and one of the reasons why I have a paid subscription. Recently I positioned a part of debt portfolio to floater funds assuming that they will be better geared to adddress rising yields. I am not nursing slight paper losses but still believe that they will be relatively more agile in the rising rate scenario than the short term or CB category. Is that correct? Any insight here is appreciated.

Yes our thesis is right. However, if rates swing due to constant intervention, then they will also be more voaltile than categories liek ultra short. Just bear that in mind. Otherwise, they will tend to be agile. thanks, Vidya

Thoroughly researched and explained well and straightforwardly. Great. Fund managers would definitely turn sharper to this new normal.

Thank you sir. Vidya

Thanks for a timely article. Specifically, could you explain:

a. Floater Funds are “accrual” in nature. They have an average duration of 1.5-2 years and probably the coupons come once every 6 months. So, the current flattish performance since mid Dec to now, would it get bumped up once the coupons come in?

b. If yes in (a), holding for a period of upto 2 years makes sense. If not, what could be the trigger for floater funds to return 6-7% p.a. over the next 2 years.

I invested in Floater basis your reco, so wanted to a deeper understanding.

FLoater funds need not be ‘accrual’ as they too reset their maturities to suit new rate scenarios. But yes, they will definitely stand to gain after some volatility from higher rates.

Yes it does. No harm in being longer too. Our reco stands but no forward looking statements on returns can be given 🙂 They will beat FD yes. thanks, Vidya

You have mentioned “categories barring overnight and liquid funds”, would you include Money Market and Arbitrage fund to this?

Money market to some extent. Arbitrage is not a debt fund. It holds some debt when arbitrage opportunity is not high thanks, Vidya

Comments are closed.